Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

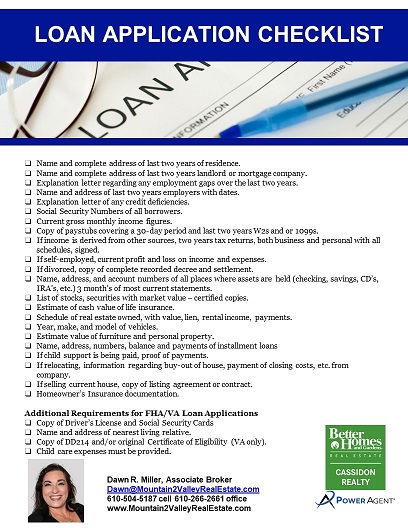

The purchase of a home is a big deal. It is one of the biggest decisions you will make in your lifetime. It can be frightening and overwhelming to even contemplate it. One of the most frequent questions I get as a Realtor is, where do I begin?

The first step in the home buying process is to contact a local lender to see what type of loan product you may qualify for and for how much.

Advantages

There are advantages to having someone local you can speak and meet with. Service can be more personalized. A local lender is more accessible. They have relationships with other real estate agents and appraisers, helping transactions go smoother. They are familiar with property values, the local economy and the nuances from one neighborhood to another.

For example, an out of state lender may not be aware of the 2% sales transfer tax Pennsylvania charges. Usually 1% is paid by the seller and 1% is paid by the buyer. However, in a multiple offer situation, a buyer may offer to pay the full 2% at closing to give them a possible advantage by saving the seller that cost. That factors into whether or not the buyer will have enough cash to close.

Local lenders are aware of other costs such as

- home owner association fees

- the cost of homeowner insurance in the area

- the threshold at which to keep the total taxes

In my own recent home search, there were a few homes I found in my price range but because of the total taxes in their location, they would have put my monthly payment at an uncomfortable level. The last thing you want is your quality of life to degrade because you are “house poor” from spending too much on housing expenses in relation to your income, leaving you short for debt repayment, savings building, time with family. What good is a house if you are always at work to pay for it?

Pre-qualification and Pre-approval

A pre-qualification is an estimate of how much money you may be able to borrow toward a home purchase. It is based on unverified information. A pre-approval is when credit checks have been run and documentation regarding your employment, income, assets and debt to income ration have been verified. A pre-approval letter from a lender allows us to sort what homes we can visit, not just by price point, but also by the type of financing. There are a variety of loan products available that will be personalized to your financial circumstances and personal preferences. There is no sense in visiting homes that only qualify for purchase by cash or with a conventional loan if you have been pre-qualified for a different loan product. This saves us all time, money, frustration and heartbreak.

You will be in position to make an offer right away with a pre-approval in hand, when you find the home that you like. This is important because there is no time for delay in today’s competitive market. A listing agent may not consider an offer valid without one. Why would a seller take their property off the market without knowing it had a solid shot to get to closing? Many agents make note on their listing that the buyer’s agent must confirm a customer is preapproved before scheduling a showing.

What if I can’t obtain financing?

Your conversation with a lender may reveal you are not in a position to purchase a home at this time. Some of the most common reasons are

- Low credit score

- Insufficient income

- Too much debt

- Deficient funds for down payment or cash to close

- Inadequate employment history

A lender can provide suggestions, resources and a timeline so you can have a clear course of action and maintain motivation in moving toward your real estate goals.

Set yourself up for success from the start by speaking with a local lender. I have a list of lenders who excel in teamwork. I am happy to share it to help you build your home buying team. You are not alone in this. I am with you all the way. Are you ready to begin?